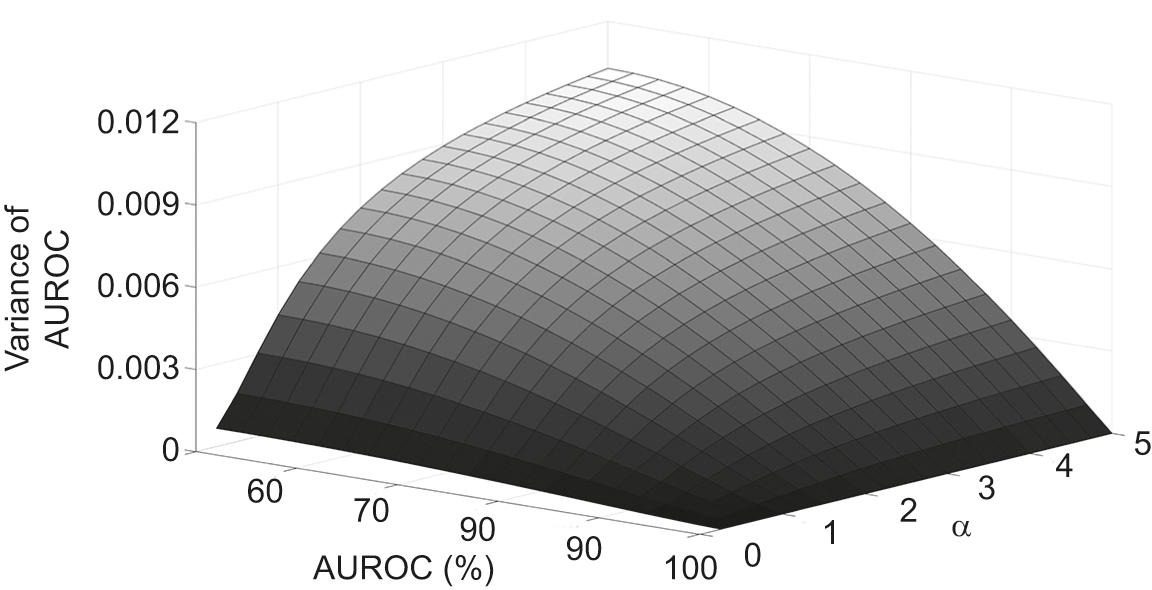

Calibration alternatives to logistic regression and their potential for transferring the statistical dispersion of discriminatory power into uncertainties in probabilities of default - Journal of Credit Risk

Por um escritor misterioso

Descrição

This paper compares four calibration approaches to linear logistic regression in credit risk estimation and proposes two new single-parameter families of

Calibration alternatives to logistic regression and their

Calibrating algorithmic predictions with logistic regression

Exposure at default models with and without the credit conversion

Probability of default (PD) news and analysis articles

PDF) The art of probability-of-default curve calibration

Exposure at default models with and without the credit conversion

Observed probabilities in logistic regression? - Cross Validated

PDF) Cost of Explainability in AI: An Example with Credit Scoring

Calibration alternatives to logistic regression and their

de

por adulto (o preço varia de acordo com o tamanho do grupo)